The Game Plan — $17

Know exactly which moves to make on each of your debts within 90 minutes — even if you have $50K+ across multiple cards.

A 128-page operating manual for the people who got the calculator readout, looked at it, and now need to know what to actually do on Monday morning. Not the book. The condensed playbook you can read in a sitting and start running tomorrow.

$17

Instant dashboard access · 128-page manual · Read in one sitting

Your cards charged you more than $17 in interest on that balance while you slept last night. This is the one $17 working to make the rest of them smaller.

Get the Game Plan — $17

30-day full refund · Author of The Debt Code (4.6★ on Amazon, 19 reviews)

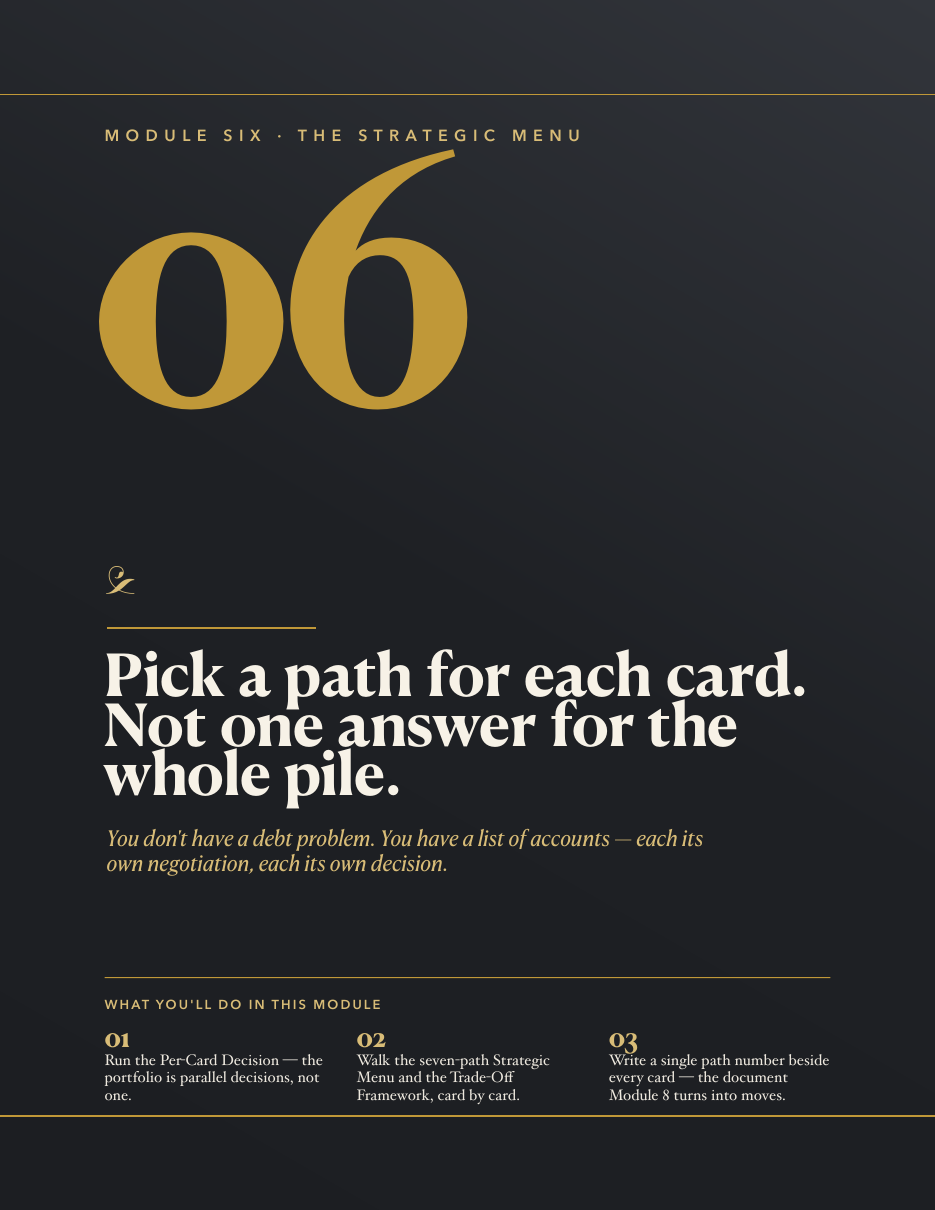

Already took the Debt Map? Your readout pointed you to specific Parts in this Game Plan.